Note for Beta Distribution

This post is out of date, please check the new post named “Beta Distribution — Intuition, Derivation, and Examples”.

1 Why Beta Distribution?

1.1 Model probabilites

The short story is that the Beta distribution can be understood as representing a distribution of probabilities, that is, it represents all the possible values of a probability when we don’t know what that probability is.

1.2 Generalization of uniform

Give me a continuous and bounded random variable, em, except the Uniform distribution. That is another way to look at beta distribution, continuous and bounded between 0, 1; also the density is not flat. \[ X \sim Beta(a, b), \text{ where } a>0, \ b>0. \]

\[ f_X(x) = c \cdot x ^{a-1}(1-x)^{b-1}, \text{ where } x>0. \]

What is \(c\)? Just a normalization constant. We’ll get the value of \(c\) later.

2 Construction

2.1 Bank and Post Office Story

Let \(X\) be the waiting time at Bank,

\[ X \sim Gamma(n_1, \lambda) \]

Let \(Y\) be the waiting time at Post Office,

\[ Y \sim Gamma(n_2, \lambda) \]

Assume \(X\) and \(Y\) are independent.

Then, what is the distribution of the proportion \(\frac{X}{X+Y}\)?

Define \(T = X+Y\) be the total waiting time.

Clearly, \(T \sim Gamma(n_1+n_2, \lambda)\), proved by MGF.

Define \(W = \frac{X}{X+Y}\) , the proportion of waiting time at Bank to the total waiting time.

What is the distribution of \(W\)?

We need to derive \(f_W(w)\), but first let’s find the joint pdf \(f_{T,W}(t,w)\) \[ \begin{align} f_{T,W}(t,w) &= f_{X,Y}(x,y) \left | \frac{\partial(x,y)}{\partial(t,w)} \right|\\ &= \frac{1}{\Gamma(n_1)}\lambda^{n_1}x^{n_1 - 1}e^{-\lambda x} \frac{1}{\Gamma(n_2)}\lambda^{n_2}x^{n_2 - 1}e^{-\lambda y} \left|-t\right| \\ &= \lambda^{n_1+n_2}t^{n_1+n_2-1}e^{\lambda t} \frac{1}{\Gamma(n_1)\Gamma(n_2)}w^{n_1 - 1}(1-w)^{n_2-1} \\ &= \frac{\lambda^{n_1+n_2}t^{n_1+n_2-1}e^{\lambda t}}{\Gamma(n_1+n_2)} \frac{\Gamma(n_1+n_2)}{\Gamma(n_1)\Gamma(n_2)}w^{n_1 - 1}(1-w)^{n_2-1}\\ &= f_T(t) \frac{\Gamma(n_1+n_2)}{\Gamma(n_1)\Gamma(n_2)}w^{n_1 - 1}(1-w)^{n_2-1} \end{align} \]

Then we find the marginal,

\[\begin{aligned} f_W(w) &= \int_0^\infty f_{T,W}(t,w) dt \\ &= \frac{\Gamma(n_1+n_2)}{\Gamma(n_1)\Gamma(n_2)}w^{n_1 - 1}(1-w)^{n_2-1} \cdot\int_0^\infty f_T(t)dt \\ &= \frac{\Gamma(n_1+n_2)}{\Gamma(n_1)\Gamma(n_2)}w^{n_1 - 1}(1-w)^{n_2-1} \end{aligned}\]Since \(f_W(w)\) is the pdf needed to be integrated to 1,

\[ \int_0^1\frac{\Gamma(n_1+n_2)}{\Gamma(n_1)\Gamma(n_2)}w^{n_1 - 1}(1-w)^{n_2-1} dw \equiv 1 \]

so the normalization constant should be

\[ c = \frac{\Gamma(n_1+n_2)}{\Gamma(n_1)\Gamma(n_2)} := \frac{1}{B(n_1, n_2)} \]

2.1.1 Summary

The connection between Gamma and Beta distribution helps us to find the normalization constant in Beta. In summary,

If \(X \sim Gamma(\alpha, \lambda)\) and \(Y \sim Gamma(\beta, \lambda)\) are independent, then \(\frac{X}{X+Y} \sim Beta(\alpha, \beta)\).

2.2 plots

library(zetaEDA)

library(ggfortify)

enable_zeta_ggplot_theme()Let’s check Beta density for some different parameters value.

How about \(a = b = 1\)? The Beta(1,1) is just the Unif(0,1).

ggdistribution(func = dbeta, x = seq(0, 1, .01), shape1 = 1, shape2 = 1) +

labs(title = "Beta Density with a = 1, b = 1")

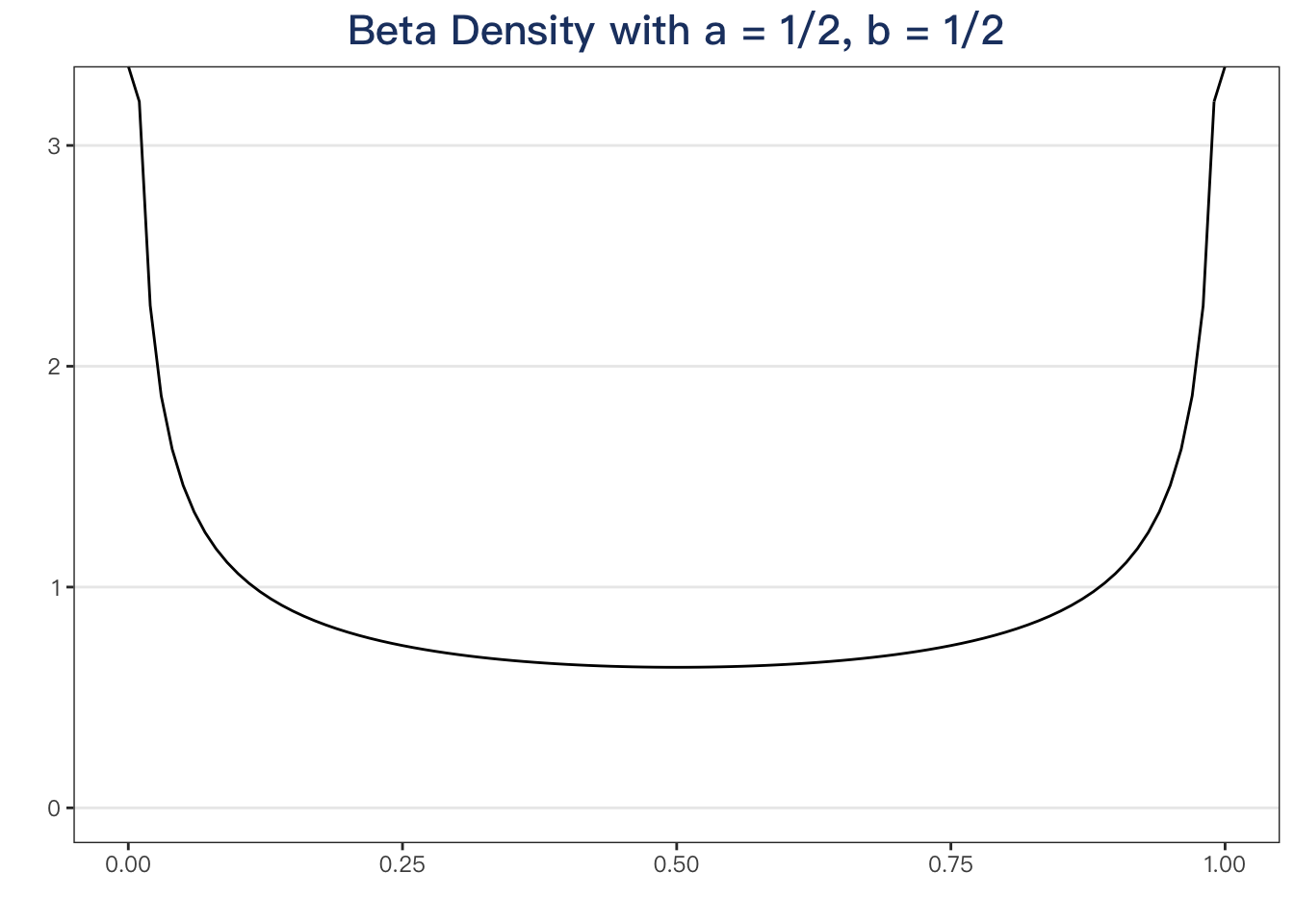

How about \(a = b = \frac{1}{2}\)?

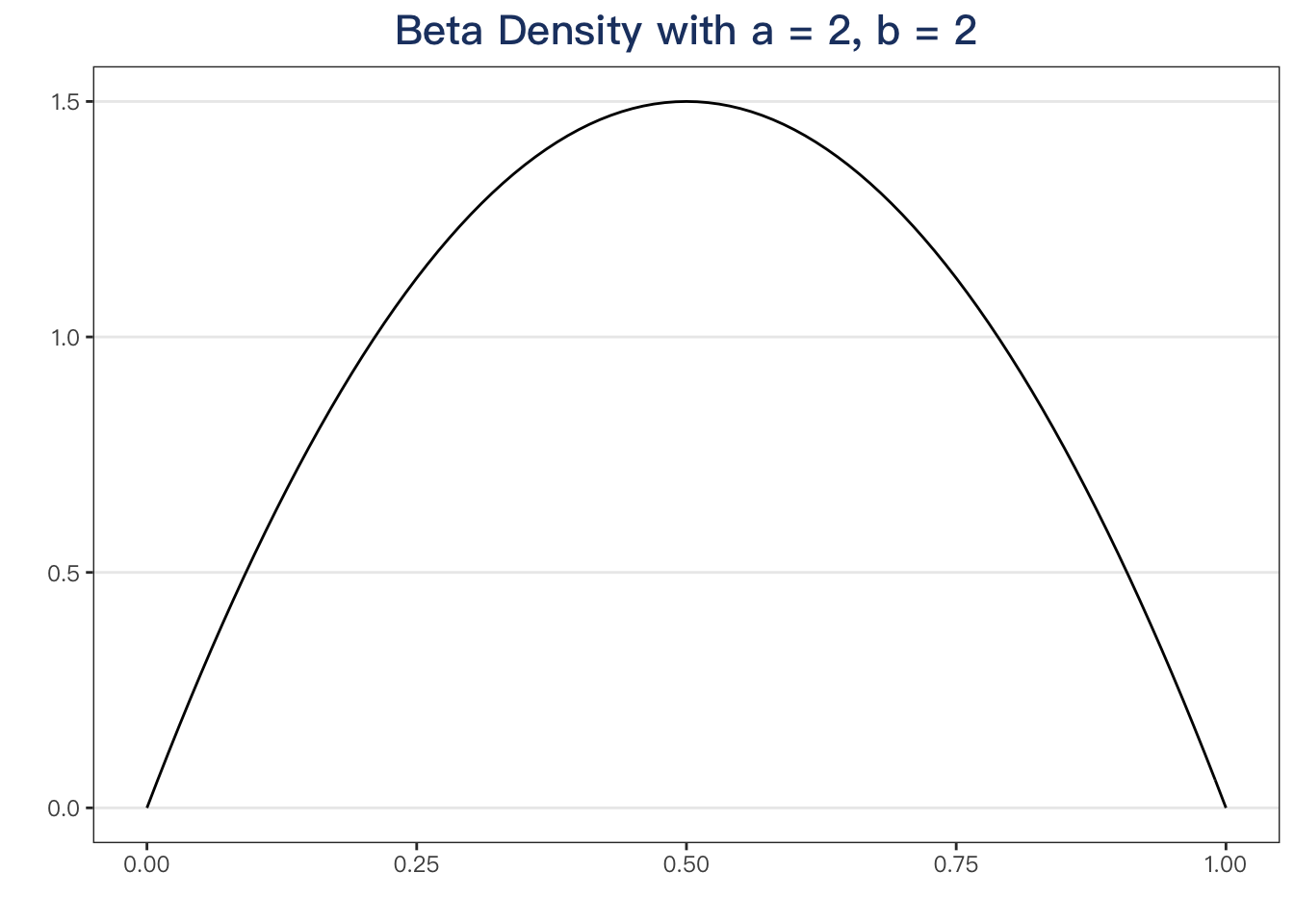

How about \(a = b = 2\)?

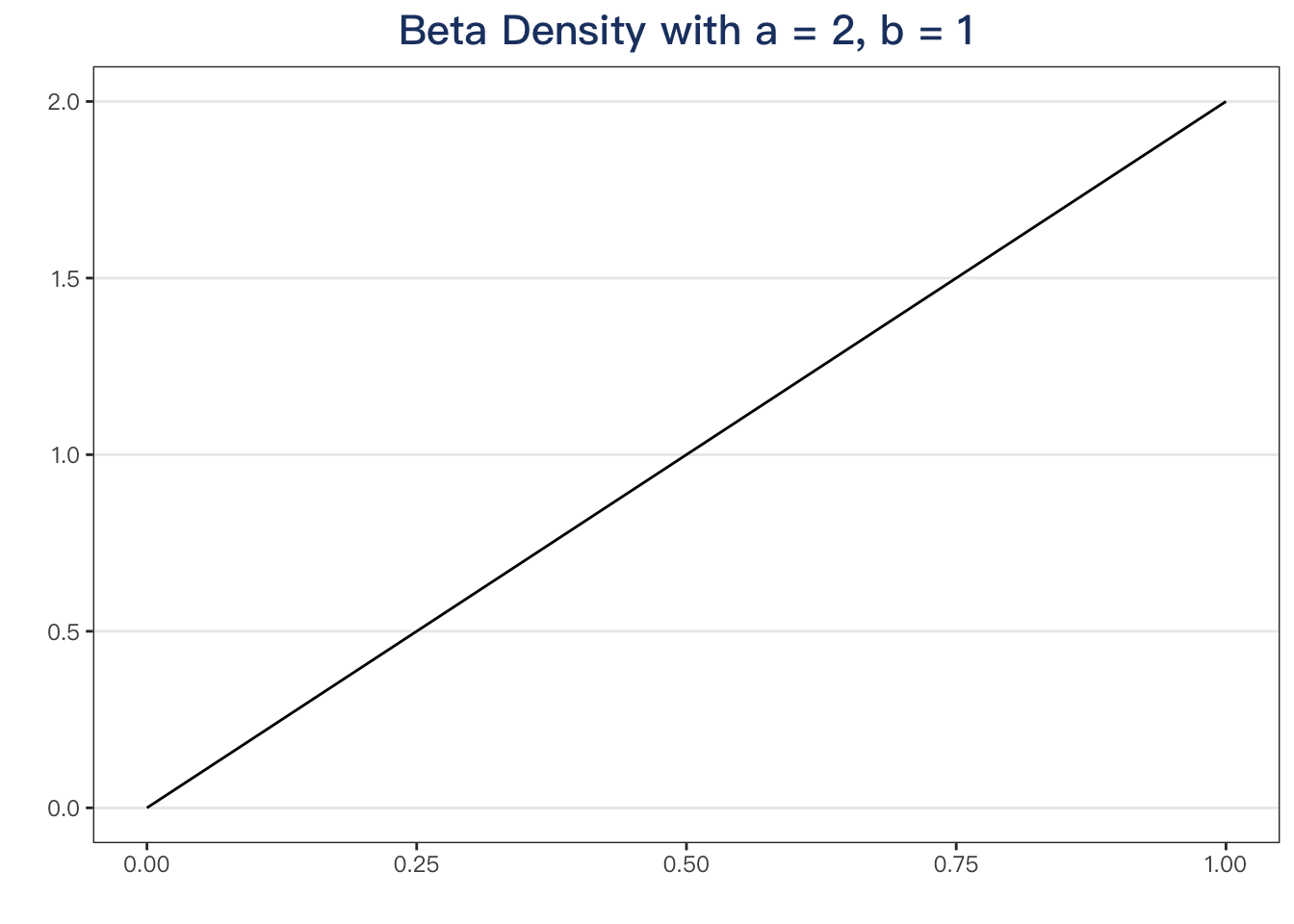

How about \(a= 2, \ b = 1\)?

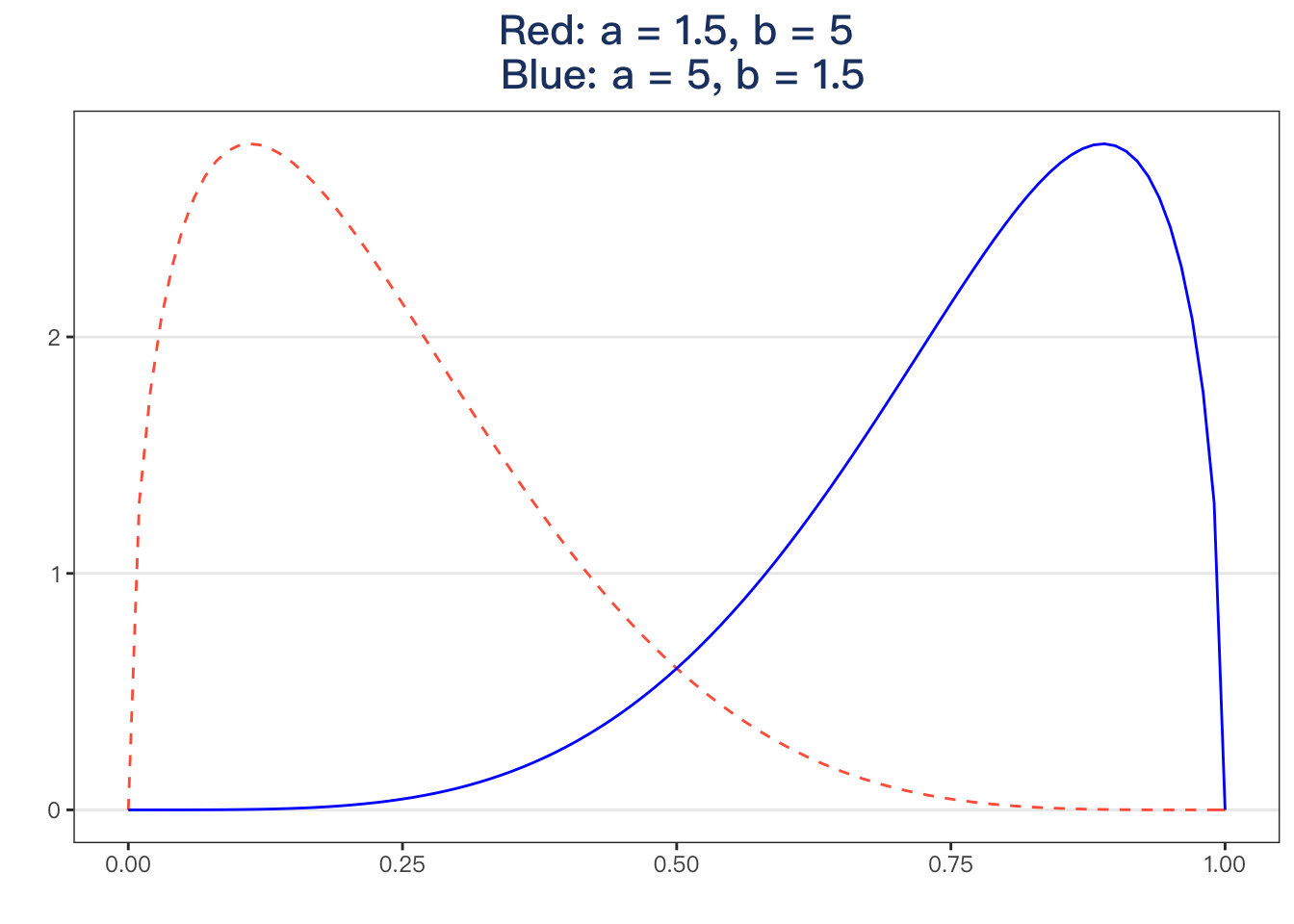

One more,

p <- ggdistribution(func = dbeta, x = seq(0, 1, .01), shape1 = 1.5, shape2 = 5, colour = "tomato", linetype = "dashed")

ggdistribution(func = dbeta, x = seq(0, 1, .01), shape1 = 5, shape2 = 1.5, colour = "blue", p = p) +

labs(title = "Red: a = 1.5, b = 5\n Blue: a = 5, b = 1.5")

For more checking, click this link and try some parameters to check the density curve.

Have fun!