Incorporating Time-Invariant Covariates into PNBD

Introducton

The original Pareto-NBD Model is awesome, but it does not allow us to add any covariates. In some cases, the covariates may affect the purchase, or the attrition process, or both. In this post, we will learn the simple case, adding the time-invariant covariates using CLVTools R package📦 and my own zetaclv package.

Next, we will predict customer’s future transactions using two approaches:

-

Divide the customers into different cohort groups, which is defined by the

first purchase year, then build the models for each cohort. -

Without “cohorting” the customer, we’ll build a model using the

first purchase yearas time-invariant covariates.

After that, let’s compare and understand the difference between two models/approaches, and choose the better one.

Add Time-Invariant Covariates in PNBD

If you familiar with the original Pareto-NBD Model (here to review), then this new model is not complicated at all!

Recall that, in PNBD Model, we assume that the transactional rate, $\lambda$, and the dropout rate, $\mu$, have the following distribution $$\lambda \sim \text{Gamma}(r, \alpha), \ \ \mu \sim \text{Gamma}(s, \beta)$$

We keep the shape parameters (i.e. $r, s$) unchanged, but replace the following scale parameters:

For more details, see Fader PS, Hardie BGS (2007). “Incorporating time-invariant covariates into the Pareto/NBD and BG/NBD models.”

Why we set $\alpha, \beta$ in this form?

The idea is from proportional hazard model (check my previous post if needed).

-

$\alpha_0, \beta_0$ refer baseline hazard.

-

The $\gamma$ part refers the log of hazard ratio.

Data Prepare

The transactional data has cust, date and sales information.

# add first purchase year column

dat <- eg_trans_data %>%

with_groups(

.groups = cust,

.f = mutate,

# first purchase year

fp_yr = min(lubridate::year(date))

) %>%

filter(fp_yr < 2020) %>%

arrange(cust, date)

# have a look

head(dat, 5) %>% print_kbl(cap = "dat")

| cust | date | sales | fp_yr |

|---|---|---|---|

| uid0001 | 2019-12-02 | 3470 | 2019 |

| uid0001 | 2020-04-20 | 1050 | 2019 |

| uid0001 | 2020-04-20 | 124 | 2019 |

| uid0003 | 2018-12-11 | 1948 | 2018 |

| uid0003 | 2019-02-22 | 828 | 2018 |

summary(dat)

## cust date sales fp_yr

## uid3414: 248 Min. :2018-01-11 Min. : 0 Min. :2018

## uid0384: 239 1st Qu.:2019-01-26 1st Qu.: 182 1st Qu.:2018

## uid1156: 191 Median :2019-08-01 Median : 560 Median :2018

## uid1149: 173 Mean :2019-09-22 Mean : 1431 Mean :2018

## uid0018: 155 3rd Qu.:2020-05-14 3rd Qu.: 1465 3rd Qu.:2019

## uid3466: 152 Max. :2021-06-07 Max. :79270 Max. :2019

## (Other):21307

We will use the fp_yr variable to define the cohort group. How many customers in each cohort?

dat %>%

group_by(fp_yr) %>%

summarize(n_cust = n_distinct(cust))

## # A tibble: 2 × 2

## fp_yr n_cust

## <dbl> <int>

## 1 2018 1097

## 2 2019 2314

Cohort Models

Cohort data:

# cohort data

dat18 <- filter(dat, fp_yr == 2018)

dat19 <- filter(dat, fp_yr == 2019)

Build the clv type of data:

dclv_18 <- generate_clvdata(

data = dat18,

splitDate = "2019-12-31"

)

## Note that: time unit is in < week >

dclv_18

## CLV Transaction Data

##

## Call:

## clvdata(data.transactions = data, date.format = "ymd", time.unit = timeUnit,

## estimation.split = splitDate, name.id = "cust", name.date = "date",

## name.price = "sales")

##

## Total # customers 1097

## Total # transactions 4968

## Spending information TRUE

##

##

## Time unit Weeks

##

## Estimation start 2018-01-11

## Estimation end 2019-12-31

## Estimation length 102.7143 Weeks

##

## Holdout start 2020-01-01

## Holdout end 2021-06-07

## Holdout length 74.71429 Weeks

dclv_19 <- generate_clvdata(

data = dat19,

splitDate = "2019-12-31"

)

## Note that: time unit is in < week >

dclv_19

## CLV Transaction Data

##

## Call:

## clvdata(data.transactions = data, date.format = "ymd", time.unit = timeUnit,

## estimation.split = splitDate, name.id = "cust", name.date = "date",

## name.price = "sales")

##

## Total # customers 2314

## Total # transactions 5108

## Spending information TRUE

##

##

## Time unit Weeks

##

## Estimation start 2019-01-01

## Estimation end 2019-12-31

## Estimation length 52.0000 Weeks

##

## Holdout start 2020-01-01

## Holdout end 2021-06-07

## Holdout length 74.71429 Weeks

Now, let’s model the cohort group data:

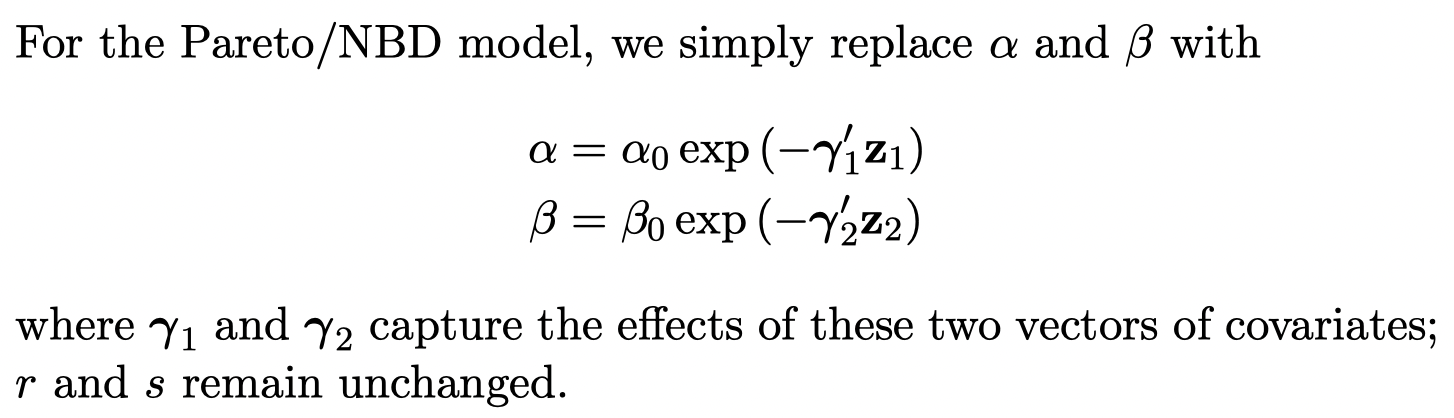

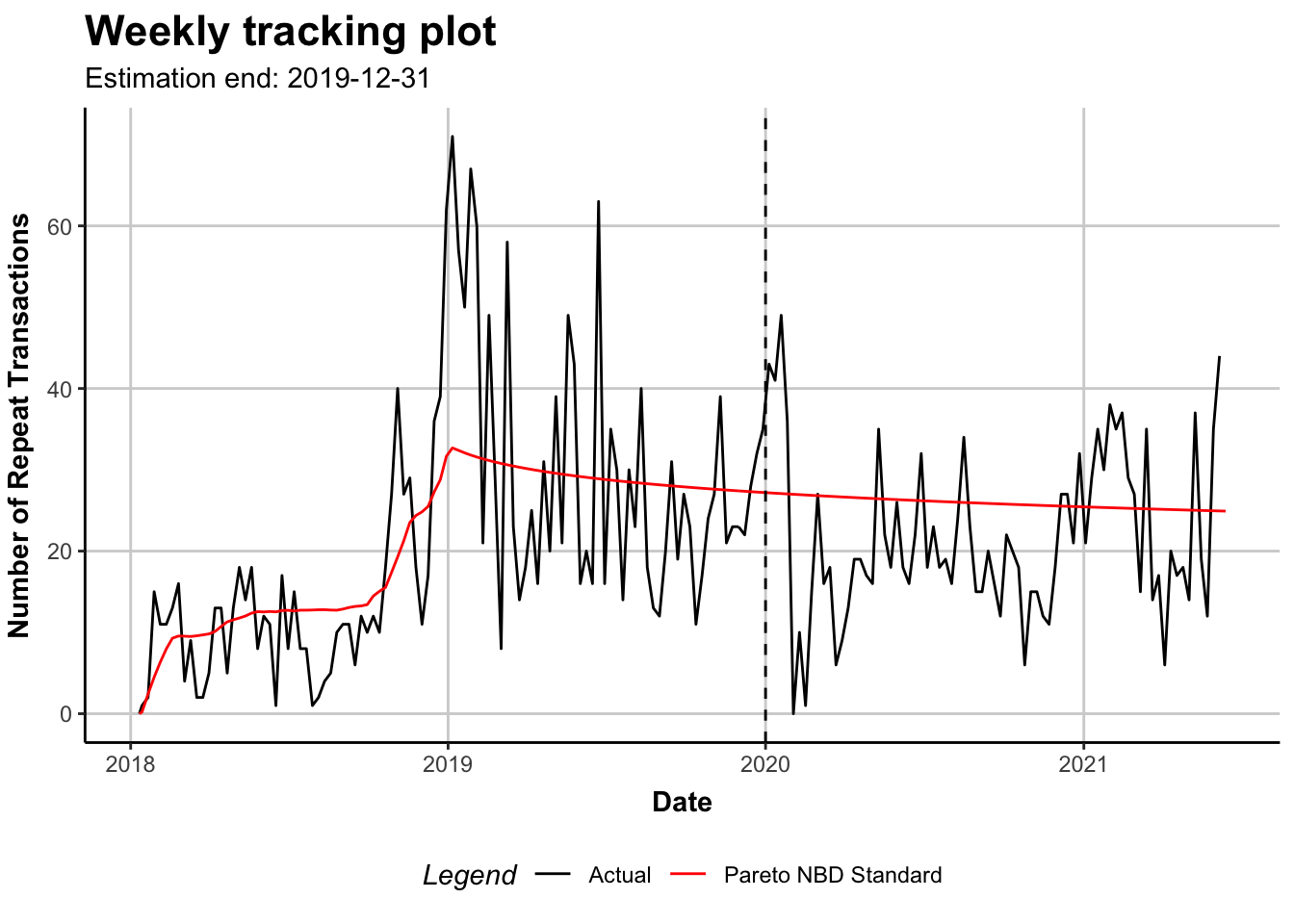

m18 <- standard_PNBD_model(dclv_18)

summary(m18)

## Pareto NBD Standard Model

##

## Call:

## pnbd(clv.data = clvData, optimx.args = optimx.args)

##

## Fitting period:

## Estimation start 2018-01-11

## Estimation end 2019-12-31

## Estimation length 102.7143 Weeks

##

## Coefficients:

## Estimate Std. Error z-val Pr(>|z|)

## r 0.39734 0.04020 9.884 < 2e-16 ***

## alpha 10.74518 1.01108 10.627 < 2e-16 ***

## s 0.12227 0.03574 3.421 0.000623 ***

## beta 2.79356 2.84873 0.981 0.326774

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Optimization info:

## LL -8303.6317

## AIC 16615.2633

## BIC 16635.2647

## KKT 1 TRUE

## KKT 2 TRUE

## fevals 195.0000

## Method Nelder-Mead

##

## Used Options:

## Correlation FALSE

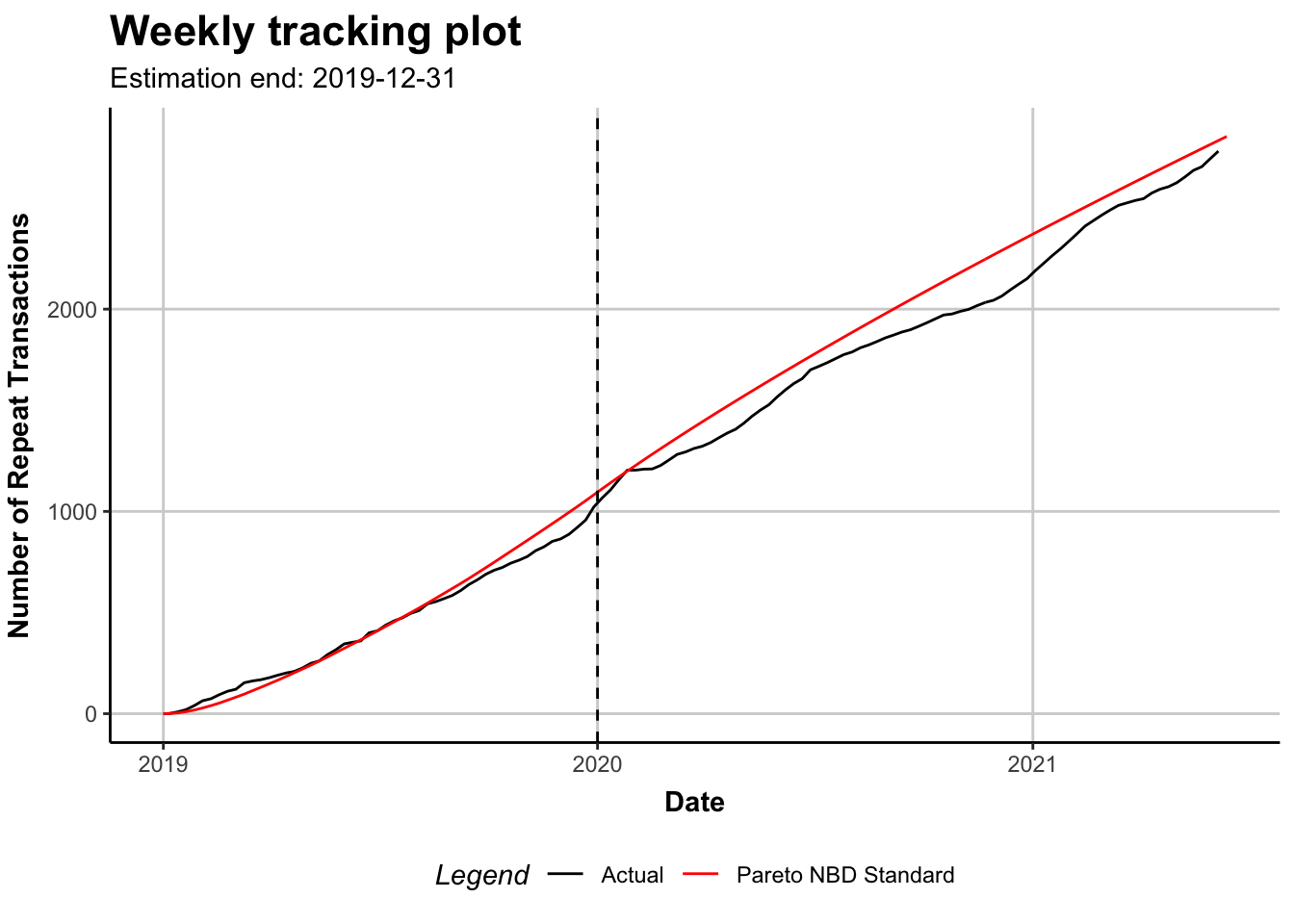

plot(m18)

plot(m18, cumulative = TRUE)

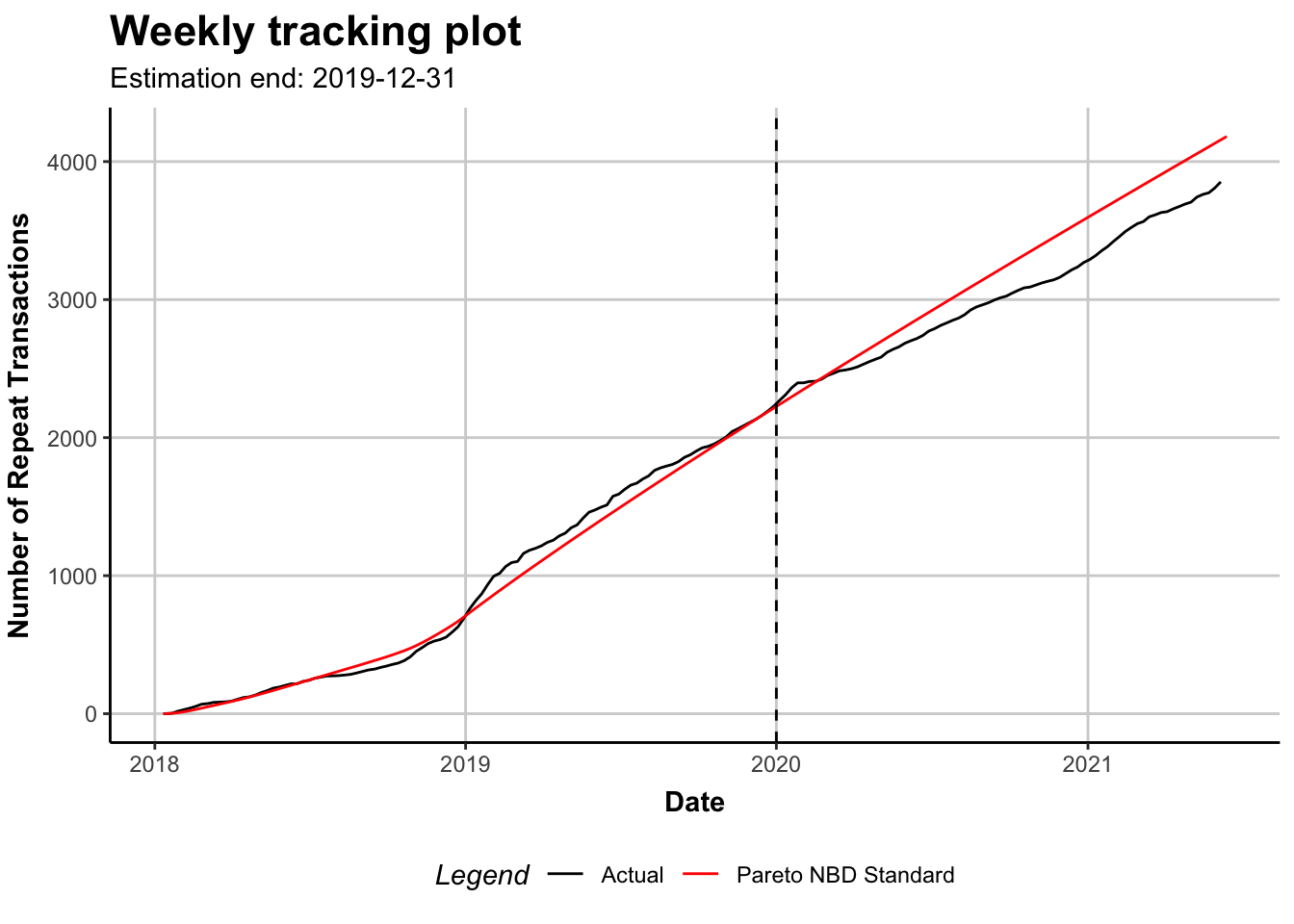

m19 <- standard_PNBD_model(dclv_19)

summary(m19)

## Pareto NBD Standard Model

##

## Call:

## pnbd(clv.data = clvData, optimx.args = optimx.args)

##

## Fitting period:

## Estimation start 2019-01-01

## Estimation end 2019-12-31

## Estimation length 52.0000 Weeks

##

## Coefficients:

## Estimate Std. Error z-val Pr(>|z|)

## r 0.44721 0.06257 7.148 8.82e-13 ***

## alpha 15.02084 1.76408 8.515 < 2e-16 ***

## s 0.26878 0.04008 6.706 1.99e-11 ***

## beta 1.08620 0.56096 1.936 0.0528 .

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Optimization info:

## LL -4778.1858

## AIC 9564.3715

## BIC 9587.3584

## KKT 1 TRUE

## KKT 2 TRUE

## fevals 489.0000

## Method Nelder-Mead

##

## Used Options:

## Correlation FALSE

plot(m19)

plot(m19, cumulative = TRUE)

compare the model coefficients:

cohort_model_coefs <- rbind(`2018` = coef(m18), `2019` = coef(m19))

cohort_model_coefs %>%

as_tibble(rownames = "cohort") %>%

print_kbl("compare the model's coef from different cohort")

| cohort | r | alpha | s | beta |

|---|---|---|---|---|

| 2018 | 0.3973431 | 10.74518 | 0.1222724 | 2.793557 |

| 2019 | 0.4472133 | 15.02084 | 0.2687787 | 1.086205 |

Interpret Coef

The expected value of transaction rate lambda is r/alpha, and the expected value of dropout rate mu is s/beta.

cohort_model_coefs %>%

as_tibble(rownames = "cohort") %>%

mutate(lambda = r / alpha, mu = s / beta) %>%

mutate(across(c(r:mu), round, digits = 3)) %>%

print_kbl("compare transaction/dropout rate")

| cohort | r | alpha | s | beta | lambda | mu |

|---|---|---|---|---|---|---|

| 2018 | 0.397 | 10.745 | 0.122 | 2.794 | 0.037 | 0.044 |

| 2019 | 0.447 | 15.021 | 0.269 | 1.086 | 0.030 | 0.247 |

We can conclude that the 2018-cohort has higher purchase rate and lower dropout rate.

Extended PNBD Model

The clv type of data:

dclv_all <- generate_clvdata(

data = dat,

splitDate = "2019-12-31"

)

## Note that: time unit is in < week >

dclv_all

## CLV Transaction Data

##

## Call:

## clvdata(data.transactions = data, date.format = "ymd", time.unit = timeUnit,

## estimation.split = splitDate, name.id = "cust", name.date = "date",

## name.price = "sales")

##

## Total # customers 3411

## Total # transactions 10076

## Spending information TRUE

##

##

## Time unit Weeks

##

## Estimation start 2018-01-11

## Estimation end 2019-12-31

## Estimation length 102.7143 Weeks

##

## Holdout start 2020-01-01

## Holdout end 2021-06-07

## Holdout length 74.71429 Weeks

The static covariate data:

stat_cov <- dat %>%

distinct(cust, fp_yr) %>%

mutate(fp_yr = factor(fp_yr, levels = c(2018, 2019)))

summary(stat_cov)

## cust fp_yr

## uid0001: 1 2018:1097

## uid0003: 1 2019:2314

## uid0004: 1

## uid0005: 1

## uid0006: 1

## uid0008: 1

## (Other):3405

The clv type of covariate data:

dclv_stat <- SetStaticCovariates(

clv.data = dclv_all,

data.cov.life = stat_cov,

data.cov.trans = stat_cov,

names.cov.life = "fp_yr",

names.cov.trans = "fp_yr",

name.id = "cust"

)

dclv_stat

## CLV Transaction Data with Static Covariates

##

## Call:

## clvdata(data.transactions = data, date.format = "ymd", time.unit = timeUnit,

## estimation.split = splitDate, name.id = "cust", name.date = "date",

## name.price = "sales")

##

## Total # customers 3411

## Total # transactions 10076

## Spending information TRUE

##

##

## Time unit Weeks

##

## Estimation start 2018-01-11

## Estimation end 2019-12-31

## Estimation length 102.7143 Weeks

##

## Holdout start 2020-01-01

## Holdout end 2021-06-07

## Holdout length 74.71429 Weeks

##

## Covariates

## Trans. Covariates fp_yr2019

## # covs 1

## Life. Covariates fp_yr2019

## # covs 1

The PNBD Model with time-invariant covariates:

ext_m <- standard_PNBD_model(dclv_stat)

summary(ext_m)

## Pareto NBD with Static Covariates Model

##

## Call:

## pnbd(clv.data = clvData, optimx.args = optimx.args)

##

## Fitting period:

## Estimation start 2018-01-11

## Estimation end 2019-12-31

## Estimation length 102.7143 Weeks

##

## Coefficients:

## Estimate Std. Error z-val Pr(>|z|)

## r 0.38211 0.02952 12.945 < 2e-16 ***

## alpha 9.36586 0.84549 11.077 < 2e-16 ***

## s 0.16033 0.03288 4.877 1.08e-06 ***

## beta 2.87077 2.27740 1.261 0.2075

## life.fp_yr2019 1.19338 0.58044 2.056 0.0398 *

## trans.fp_yr2019 -0.52757 0.11754 -4.489 7.17e-06 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

##

## Optimization info:

## LL -13095.4075

## AIC 26202.8149

## BIC 26239.6235

## KKT 1 TRUE

## KKT 2 TRUE

## fevals 607.0000

## Method Nelder-Mead

##

## Used Options:

## Correlation FALSE

## Regularization FALSE

## Constraint covs FALSE

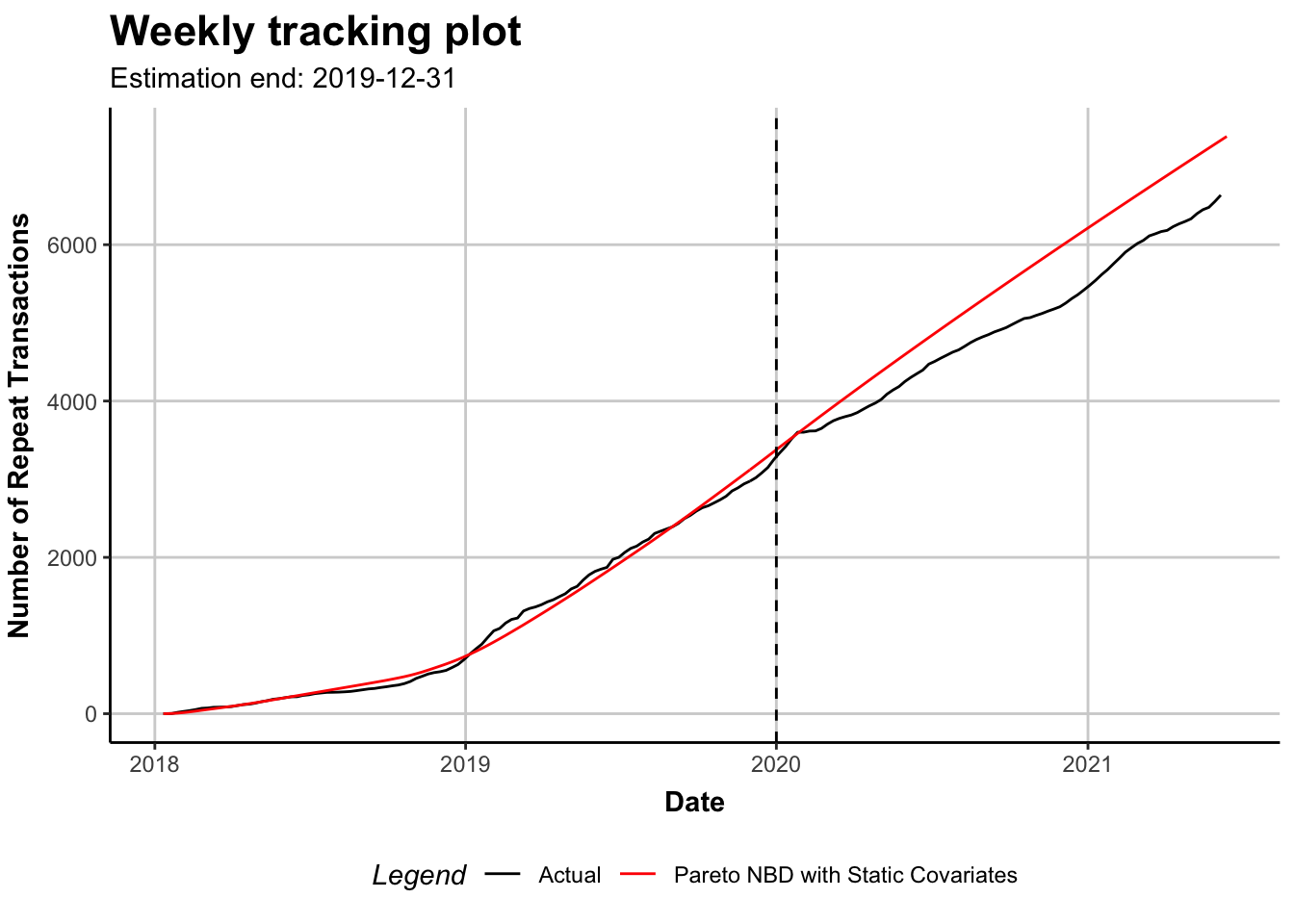

plot(ext_m, cumulative = TRUE)

Interpret Coef

coef(ext_m) %>%

enframe(name = "coef")

## # A tibble: 6 × 2

## coef value

## <chr> <dbl>

## 1 r 0.382

## 2 alpha 9.37

## 3 s 0.160

## 4 beta 2.87

## 5 life.fp_yr2019 1.19

## 6 trans.fp_yr2019 -0.528

Note that, the baseline or “reference group” is cohort-2018, and we already know its 4 parameters.

For cohort-2019,

-

The cohort-2018 and cohort-2019 share the same values of

rands. -

We only need to find its

alphaandbeta.

Plug into the formula: alpha = alpha0 * exp(-gamma1 * z1) and beta = beta0 * exp(-gamma2 * z2)

coefs <- unname(coef(ext_m))

# for cohort-2018, as reference group

r <- coefs[1]

s <- coefs[3]

alpha0 <- coefs[2]

beta0 <- coefs[4]

# here, the covariates are indicator variables (0/1; 0 refers baseline)

z1 <- 1

z2 <- 1

# gamma

gamma1 <- coefs[6]

gamma2 <- coefs[5]

# for cohort-2019

alpha <- alpha0 * exp(-gamma1 * z1)

beta <- beta0 * exp(-gamma2 * z2)

# put all together

coef_tbl <- tibble(

r = c(r, r),

alpha = c(alpha0, alpha),

s = c(s, s),

beta = c(beta0, beta)

) %>%

mutate(cohort = c(2018, 2019), .before = 1) %>%

mutate(

lambda = r / alpha,

mu = s / beta

)

coef_tbl %>%

mutate(across(r:mu, round, digits = 3)) %>%

print_kbl(

highlight_cols = c("lambda", "mu"),

cap = "compare transaction/dropout rate"

)

| cohort | r | alpha | s | beta | lambda | mu |

|---|---|---|---|---|---|---|

| 2018 | 0.382 | 9.366 | 0.16 | 2.871 | 0.041 | 0.056 |

| 2019 | 0.382 | 15.873 | 0.16 | 0.870 | 0.024 | 0.184 |

Compare Two Models

The following tables show the values of coefficients from two models:

| cohort | r | alpha | s | beta | lambda | mu |

|---|---|---|---|---|---|---|

| 2018 | 0.397 | 10.745 | 0.122 | 2.794 | 0.037 | 0.044 |

| 2019 | 0.447 | 15.021 | 0.269 | 1.086 | 0.030 | 0.247 |

| cohort | r | alpha | s | beta | lambda | mu |

|---|---|---|---|---|---|---|

| 2018 | 0.382 | 9.366 | 0.16 | 2.871 | 0.041 | 0.056 |

| 2019 | 0.382 | 15.873 | 0.16 | 0.870 | 0.024 | 0.184 |

According to above results, both Cohort Model and Extended PNBD Model have the same conclusion that cohort-2018 is better, which has the higher purchase rate and lower dropout rate.

The time unit used in the models is week. Now let’s change the time unit to year and try to get more intuitive result (i.e. compare the average number of transactions in a year, lambda, etc.).

| cohort | lambda | mu |

|---|---|---|

| 2018 | 1.92 | 2.28 |

| 2019 | 1.55 | 12.87 |

| cohort | lambda | mu |

|---|---|---|

| 2018 | 2.12 | 2.90 |

| 2019 | 1.25 | 9.58 |

Compare Prediction Accuracy

Now let’s compare two models’ prediction error for CET (conditional expected transactions).

-

CET = PAlive * updated mean of Pareto/NBD

-

The value of CET has already involved the probability of alive (PAlive)!

ext_pred <- predict(ext_m)

ext_err <- ext_pred %>%

summarize(

MAE = mean(abs(actual.x - CET)),

RMSE = sqrt(mean((actual.x - CET)^2))

)

ch18_pred <- predict(m18) %>%

select(actual.x, CET)

ch19_pred <- predict(m19) %>%

select(actual.x, CET)

ch_err <- bind_rows(ch18_pred, ch19_pred) %>%

summarize(

MAE = mean(abs(actual.x - CET)),

RMSE = sqrt(mean((actual.x - CET)^2))

)

bind_rows(

ch_err,

ext_err

) %>%

mutate(type = c("cohort model", "ext PNBD"), .before = 1) %>%

print_kbl(cap = "Compare Model Prediction Error")

| type | MAE | RMSE |

|---|---|---|

| cohort model | 1.031840 | 2.585261 |

| ext PNBD | 1.070709 | 2.623130 |

In this case, the cohort model is slightly more accurate in terms of MAE and RMSE.

However, in practice we may deal with many cohort groups and thus have to build many models. At that time, the extended PNBD with time-invariant covariate may save you a lot of time.

For example, in the above story, we used the first purchase year as time-invariant covariates to build ONLY ONE model instead of building m18 and m19, 2 separate models for 2018/2019 cohort groups.

Of course, there is no free lunch. We always need to balance the degree of “convenience” and the prediction accuracy.

Reference

-

Fader PS, Hardie BGS (2007). “Incorporating time-invariant covariates into the Pareto/NBD and BG/NBD models.” URL http://www.brucehardie.com/notes/019/time_invariant_covariates.pdf.